All Categories

Featured

Table of Contents

[/image][=video]

[/video]

Presuming rates of interest stay strong, even greater assured rates could be feasible. It refers what terms finest fit your investment requirements. We tailor several techniques to make best use of growth, earnings, and returns. Utilizing a laddering technique, your annuity portfolio renews every number of years to maximize liquidity. This is a sensible method in today's increasing rate of interest rate environment.

Rates are ensured by the insurance company and will neither raise nor reduce over the selected term. We see passion in temporary annuities using 2, 3, and 5-year terms.

Annuity Appointments

Which is best, easy rate of interest or worsening interest annuities? The solution to that depends upon exactly how you use your account. If you don't intend on withdrawing your rate of interest, after that generally offers the highest possible prices. A lot of insurer just offer intensifying annuity plans. There are, however, a couple of policies that debt simple passion.

It all depends on the hidden rate of the dealt with annuity agreement, of training course. Experienced repaired annuity financiers know their premiums and passion gains are 100% available at the end of their selected term.

Unlike CDs, dealt with annuity policies enable you to withdraw your interest as revenue for as lengthy as you wish. And annuities supply higher prices of return than nearly all similar bank instruments supplied today. The various other item of excellent news: Annuity prices are the highest possible they have actually been in years! We see considerably more passion in MYGA accounts currently.

They generally provide far better returns than financial institution CDs. With boosting rate of interest comes competitors. There are numerous very rated insurance provider trying deposits. There are several popular and highly-rated firms supplying competitive yields. And there are agencies focusing on rating annuity insurance provider. You can want to AM Ideal, COMDEX, Moody's, Criterion and Poor's, Fitch, and Weiss amongst others.

Insurance firms are commonly risk-free and safe establishments. A couple of that you will see above are Dependence Requirement Life, sister firms Midland and North American Life, Americo, Oxford Life, American National, Royal Neighbors, Pacific Guardian Life, Athene, Sagicor, Global Atlantic, and Aspida to name a few.

They are risk-free and reputable plans designed for risk-averse investors. The financial investment they most very closely resemble is certifications of deposit (CDs) at the financial institution. Watch this brief video clip to understand the resemblances and distinctions between the two: Our customers buy dealt with annuities for a number of reasons. Safety and security of principal and assured rates of interest are absolutely 2 of one of the most important aspects.

Annuities Inflation Adjusted

These policies are very versatile. You might intend to defer gains currently for bigger payouts during retirement. We offer items for all situations. We help those requiring instant rate of interest revenue now as well as those preparing for future revenue. It is essential to note that if you require income currently, annuities function best for those over age 59 1/2.

Why function with us? We are an independent annuity broker agent with over 25 years of experience. We are accredited with all providers so you can shop and contrast them in one area. Rates are scooting and we do not know what's on the perspective. We aid our customers lock in the highest possible yields feasible with risk-free and secure insurer.

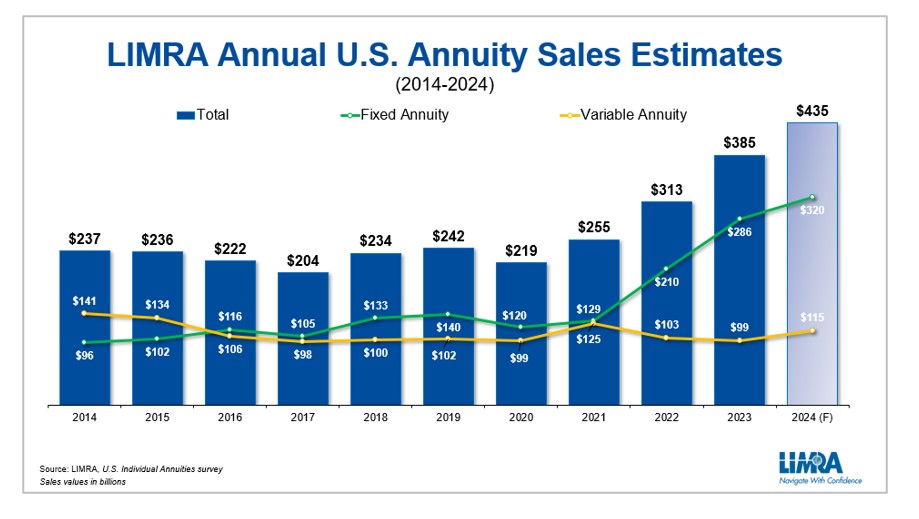

In recent times, a wave of retiring baby boomers and high interest rates have helped gas record-breaking sales in the annuity market. From 2022 to 2024, annuity sales topped $1.1 trillion, according to Limra, an international research study company for the insurance policy industry. In 2023 alone, annuity sales enhanced 23 percent over the prior year.

Annuity Transfers

With even more potential rate of interest price cuts on the horizon, straightforward fixed annuities which often tend to be much less complicated than various other options on the marketplace may become much less interesting consumers because of their winding down rates. In their place, other selections, such as index-linked annuities, might see a bump as consumers seek to capture market development.

These price walks provided insurance provider space to offer more attractive terms on repaired and fixed-index annuities. "Rates of interest on fixed annuities also climbed, making them an attractive investment," says Hodgens. Also after the stock exchange rebounded, netting a 24 percent gain in 2023, lingering worries of an economic crisis maintained annuities in the limelight.

Other aspects also contributed to the annuity sales boom, consisting of more financial institutions now providing the products, says Sheryl J. Moore, Chief Executive Officer of Wink Inc., an insurance coverage marketing research firm. "Customers are becoming aware of annuities more than they would certainly've in the past," she says. It's likewise easier to purchase an annuity than it made use of to be.

"Literally, you can obtain an annuity with your agent through an iPad and the annuity is accepted after completing an on the internet form," Moore claims. "It made use of to take weeks to obtain an annuity via the concern procedure." Fixed annuities have actually moved the recent growth in the annuity market, representing over 40 percent of sales in 2023.

Limra is expecting a pull back in the appeal of taken care of annuities in 2025. Sales of fixed-rate deferred annuities are expected to drop 15 percent to 25 percent as rates of interest decrease. Still, repaired annuities have not shed their sparkle quite yet and are offering traditional financiers an attractive return of even more than 5 percent in the meantime.

Americo Annuities

There's also no need for sub-accounts or profile monitoring. What you see (the promised price) is what you obtain. On the other hand, variable annuities frequently include a laundry checklist of costs death costs, management costs and financial investment management charges, among others. Set annuities maintain it lean, making them a simpler, cheaper choice.

Annuities are complicated and a bit various from other monetary products. Discover just how annuity costs and payments work and the common annuity terms that are useful to understand. Fixed-index annuities (FIAs) broke sales records for the third year straight in 2024. Sales have almost doubled given that 2021, according to Limra.

Caps can vary based on the insurance firm, and aren't most likely to stay high for life. "As interest prices have been coming down lately and are anticipated to come down additionally in 2025, we would anticipate the cap or involvement prices to also boil down," Hodgens states. Hodgens anticipates FIAs will stay eye-catching in 2025, yet if you remain in the market for a fixed-index annuity, there are a couple of points to enjoy out for.

In theory, these hybrid indices aim to smooth out the highs and lows of a volatile market, but in reality, they've typically dropped brief for customers. "Numerous of these indices have returned little to absolutely nothing over the past couple of years," Moore says. That's a hard tablet to swallow, considering the S&P 500 uploaded gains of 24 percent in 2023 and 23 percent in 2024.

Variable annuities when dominated the market, but that's transformed in a big means. These products experienced their worst sales on record in 2023, dropping 17 percent contrasted to 2022, according to Limra.

Silac Annuity Reviews

Unlike taken care of annuities, which use drawback security, or FIAs, which balance security with some development possibility, variable annuities give little to no protection from market loss unless motorcyclists are added at an included expense. For capitalists whose top priority is protecting resources, variable annuities merely do not measure up. These products are likewise infamously complicated with a history of high fees and hefty abandonment costs.

Yet when the marketplace broke down, these bikers became liabilities for insurers due to the fact that their guaranteed values exceeded the annuity account values. "So insurance provider repriced their cyclists to have less appealing functions for a greater rate," says Moore. While the industry has made some efforts to improve transparency and lower expenses, the product's past has actually soured numerous customers and financial experts, that still see variable annuities with apprehension.

Benefit Base Annuity

RILAs offer customers much higher caps than fixed-index annuities. Exactly how can insurance business pay for to do this?

For instance, the wide variety of attributing methods made use of by RILAs can make it tough to compare one product to an additional. Higher caps on returns additionally come with a compromise: You take on some danger of loss beyond an established floor or barrier. This barrier shields your account from the first section of losses, usually 10 to 20 percent, however afterwards, you'll shed cash.

{kind=link}

Table of Contents

Latest Posts

Annuity Vanguard

Lv Annuity

Raymond James Annuities

More

Latest Posts

Annuity Vanguard

Lv Annuity

Raymond James Annuities